Forensic Fundamentals

Highlighting fraud, cybercrime and forensic accounting issues from the fundamentals to advanced.

Is your company large or listed?

The importance of the expert witness role continues to hold its place in the arena of law. Ultimately, our role as experts is always to assist the Court. In particular, our role is to help the Judge reach a judgement they consider fair and equitable based upon the opinion offered by an expert, or experts, where the Judge may prefer the opinion of one over the opinion of another. It all boils down to evidence, reasoned arguments, and opinion.

The expert role will typically only be required where additional information is needed by the Court. If the matter can be dealt with by reference to the law alone it will likely not be needed, perhaps for civil matters such as a tenancy dispute or a contractual wrangle. Or rather, one of the Parties might apply to the Court to argue expert evidence is needed to allow the Judge to make an appropriate and fair judgement. This will be most relevant in areas such as medicine, accountancy, architecture and similar. The expert’s role can be summarised as follows: it is to clarify and simplify potentially complex issues within their field; and to provide objective opinion that is unswayed by those instructing or paying them.

However, by the very nature of how experts are appointed, with a party approaching them with a scope of work and typically agreeing a daily rate for the work to be carried out, there may be a subliminal leaning to seek a high bar (when acting for the Claimant) or to minimise the quantum of a claim (when acting for the Defendant). It is the strong expert who will advise a party, possibly seeking a high worth claim, that there will be little to no chance of success and to save their money. This may not be the news a client wants to hear, but anything less than presenting a case from an independent perspective will not help the client, or expert’s reputation, in the long term.

One of the processes designed to assist the Court is the joint statement – whereby experts look to narrow the issues they disagree on in a single standalone report – however this can sometimes turn out to be the ground where each party simply expands on the reasons they disagree with the other expert, which is of no assistance to the Court in reaching its judgment.

Many criminal matters may require a jury to decide the fate of a defendant, without any expert input. In other cases, there may be matters such as the Lucy Letby trial where expert medical evidence forms the heart of the case and which continues to draw media speculation for the roles of the experts in determining the guilt of the defendant, raising important topics around over reliance on limited expert findings, and the adequacy of ‘common juries’ in assessing complex industry evidence.

Experts are in a unique position, whereby they can support a client throughout all stages of a case matter, from initial advisory work, where Court proceedings may never even be envisaged, through to giving evidence in Court.

There is also the possibility of providing advice in any alternative dispute resolution process, be that at mediation (where cases sometimes settle) or some of form of expert determination, where the expert will effectively preside as ‘judge’ under joint instructions from both parties with rounds of submissions provided for their review.

Did you know…If an expert gives an opinion without any substantive evidence to support it, they can become the target of criticism from a Judge in their ruling which can seriously harm their reputation. If you would like more information on our expert witness services, please visit Forensic Services, or contact Martin Chapman and Alex Houston. |

Divya Devadoss, Associate Director, Forensic Services

As the corporate landscape becomes ever more complex with more convoluted organisational structures and reporting rules, the risk related to related parties increases.

A related party is a person or organisation that has a close relationship with a reporting entity, including close family members, subsidiaries, affiliates and entities controlled by related individuals. Such individuals or entities could influence or be influenced by the financial or operational decisions of the reporting entity. Related party entities can therefore pose serious audit and fraud risks, especially when used to manipulate financial statements or conceal misconduct.

In the first instance, identifying all related parties can be difficult. Management may fail to disclose all related parties, making it difficult for auditors to identify and assess the impact. This can be particularly difficult as the definition of related parties can be complex and is not always fully understood by management and related parties are often undisclosed in good faith.

Transactions with related parties are inherently risky because they often lack the independence and transparency of arm's-length dealings.

Key risks include:

These risks are exacerbated when internal controls are weak or when transactions occur outside the normal course of business. Auditing standards like ISA 550 require auditors to scrutinise related party transactions for legitimacy, business rationale, and proper disclosure.

This can have serious consequences for auditors. In one high-profile case, the Financial Reporting Council (FRC) issued a fine of over £1.3 million in relation to audit failures involving undisclosed related party transactions. A key finding was the lack of professional scepticism applied to management’s assertion that a delivery company, reportedly controlled by a close relative of the CEO, was not a related party. The case underscores the importance of rigorous scrutiny and proper disclosure in related-party dealings.

Forensic accountants bring a specialised skill set to uncover and mitigate fraud risks associated with related party entities. Their contributions include.

Identifying hidden relationships

Analysing transactions for fraud

Evaluating internal controls

Supporting legal and regulatory action

While related party entities are a normal part of business operations, they require rigorous audit procedures and forensic scrutiny to ensure they are not misused. By combining investigative techniques with financial expertise, forensic accountants help organisations maintain integrity, comply with regulations, and protect stakeholder interests. The Crowe Forensic Team handles a substantial number of forensic cases, varying in size and complexity. We are always happy to have an initial, no-obligation discussion on any matters where we can add value and provide expert advice. For more information, please contact Alex Houston or your usual Crowe contact.

Forensic expert witnesses are often involved in determining the profits lost because of the actions of another party. This is typically termed a loss of profit claim or, if the business has been discontinued for a period, a business interruption claim.

This can be viewed from the perspective of the party that has suffered the loss (Claimant), or the party that has allegedly caused the loss (Defendant).

Whether defending or assisting in formulating the claim, a primary aim of the expert witness is to gain a sound understanding of the business. For instance, is it a manufacturing or service business, does it serve overseas markets, is it a seasonal business, and so on. The expert witness should also gain an understanding of how the business generates its revenues and profit streams. This will lie at the heart of determining the loss suffered.

The reporting aim is to quantify the position a business would have been in but for the actions of the Defendant, often described as the ‘But For’ Position.

It is important to consider each case on its own merits and what has taken place, for example:

Typically, when instructed by a Claimant, the above information will be collated and, in conjunction with discussions with company management and independent review of the financial evidence, an expert report will be disclosed to the Court to assist in the determination of damages.

When acting for the Defendant, there would typically be a schedule of loss already disclosed within proceedings. This schedule represents the main focus in assisting the Defendant to assess the claim, as a review of this can unveil fundamental flaws in the case being brought against them.

One common area for all loss of profit cases is the matter of causation, that is, whether there is an identifiable link between a certain event, allegedly caused by the defending party, and the resulting loss of profit. A Claimant will typically point to a tail off in business, with declining revenue and profit streams, arising as a direct cause of the other party’s actions.

It can be the case, however, that any dip in a business’s performance is not necessarily a direct reflection of the actions of the other party, but is instead a result of trading conditions or events that lie outside the responsibility of the Defendant.

Part of the above review might also look more granularly at a business, breaking down its fixed and variable overheads. Certain costs will vary according to the volume of business, but costs such as rent, or rates, generally will not.

With every loss suffered, it is the responsibility of the Claimant to mitigate their loss; that is, to undertake reasonable actions to minimise the loss that it suffers. For example, could trade have continued on a different production line, or certain work been sub-contracted out to allow it to continue in some form and so minimise losses arising.

There can also be situations where a business actually does better as a result of an incident. Take the example of certain shops during Covid experiencing a surge in online sales and profitability as they stopped incurring property costs.

Did you know…In certain cases, a poorly formulated case or providing inappropriate or misleading evidence can see a party ordered to pay the other side’s professional costs of attending trial. |

Most importantly, it must be borne in mind that, whether acting on behalf of the Claimant or the Defendant on reviewing the loss of profit claim, an expert’s duty is to the Court rather than the party paying or instructing them. They must be seen to be acting impartially, and from an independent perspective, not impacted by the wishes and motivations of the client.

If you would like more information on our expert witness services, please contact Martin Chapman, Alex Houston or your usual Crowe contact.

As a party appointed expert, your instructions come from one of the two parties (or possibly multi parties) that are in dispute, you will either be instructed directly by that party or (more commonly) by the solicitors acting as agent for that party – you may be acting for the party that ‘holds the information’ (e.g. the company’s remaining majority shareholders following a minority exit) or for the party that might not have as much access to information i.e. the exiting minority shareholder) – whichever party appoints you, however, your core responsibility and overriding duty is to the court - you must remain independent and be seen to be independent - the solicitor and barrister are advocates for their client, while the expert is there to give an independent opinion on accounting matters that lie within their expertise.

As an SJE, you are jointly instructed by both parties, this can actually take place in both ‘amicable’ and ‘confrontational’ scenarios, whereby friendly parties wanting to reach a settlement may agree to equally bear the costs of one expert; and similarly, where the parties are not on amicable terms, they may actually agree that their opinions are so polarised that it makes more sense to jointly appoint just the one independent expert to opine on the matter they are arguing over – however, if either party does not wish to show any form of ‘friendly’ co-operation then they are always more likely to appoint a party appointed expert, possibly in the mistaken belief that they may favour their position.

A common scenario arising from an SJE appointment is the position whereby a ‘shadow’ expert is appointed – this will be an instruction to review the work of the SJE and, although you are not part of the formal court process, your advice will be provided on the merits of the SJE report and where any questions may be raised on specific points.

An expert determination will usually come through an institute like the ICAEW, when parties cannot reach an agreement but do not wish to revert to long and expensive litigation – two rounds of submissions will be made by each party (their original arguments followed by their comments on the other side’s argument) and the expert witness will make a determination that is intended to draw a line under the matter and provide closure for the parties. Alternatively, we can provide advice to a party making their submissions.

In an advisory role the expert might typically be giving provisional advice as to the merits of pursuing a case, advice on how to calculate quantum, or reviewing the merits of a claim that a party is facing – this information would only be made available to the instructing party and would not be admitted into court.

Did you know…In whatever expert role you undertake, you must maintain your independence and base your opinions on the evidence available rather than the entrenched position of the party instructing or paying you. |

For more information, please contact Martin Chapman or your usual Crowe contact.

The preparation of an expert witness report is a crucial process, allowing the expert to assist the court by clearly summarising findings within their area of expertise.

Below is a summary of key information regarding the layout and content of these reports.

An expert witness report should provide a concise statement of facts and assumptions used by the expert. It is important that the reader can easily follow the expert’s reasoning leading to the conclusions reached. Any technical matters should be explained in terms that an intelligent layperson can understand. Additionally, the expert should include a summary of the instructions they received to avoid any potential misunderstandings.

The report will serve as the primary piece of evidence provided by the expert to the court. As such, the Civil Procedure Rules (CPR) clearly outline what must be included in an expert’s report. It is essential to show that the expert is presenting their own independent professional opinion. Moreover, the CPR makes it clear that the expert’s overriding duty is to the court, not to the party who appoints or compensates them.

Did you know…An expert may be employed in various capacities, including, arbitration, tribunals, and litigation. |

For more information on the forensic accounting services we offer, please contact Martin Chapman.

What better way for forensic accountants to get into the spirit of the Olympics than with an article intertwined with Olympic facts. Starting with fact number one which also provides an admittedly slightly tenuous link to expert determinations.

Did you know…The Olympic motto is “Faster, Higher, Stronger – Together”, with “Together” being a recent addition in 2021, to recognise that we can only go faster, aim higher and become stronger by standing together in solidarity. |

Expert determinations can be faster, higher, and stronger than other forms of dispute resolution. For more details on expert determinations, please see our other articles on What is an Expert Determination and Top 10 tips for a successful expert determination. However, in summary, this is a binding form of dispute resolution, usually used in a matter that is technical in nature (such as accountancy). An expert is jointly appointed by disputing parties to provide their expert determination to resolve the dispute.

Expert determinations are usually much faster than disputes that adopt more traditional legal claim processes. From the point of an expert being instructed, the matter can be resolved in as little as 20 to 30 business days. A typical timetable might be that the parties have five to 10 business days to submit their position to the expert, a further five business days for the parties to respond to each other’s submissions and then 10 to 15 business days for the expert to reach their determination. This process is flexible however, as the timetable and submission process can be adapted according to the needs and complexity of the matter.

Did you know…In the 2008 Beijing Olympics Usain Bolt won the 100m in a world record time of 9.69 seconds, despite his shoelace being untied. |

Expert determinations can often result in the successful party retaining a higher amount of any award granted. This is because the process can be highly cost-effective, as the parties typically share the costs of the expert determiner. This straightforward process means that there is minimal back and forth correspondence between the parties, and no need for an expensive trial in court, should alternative dispute resolution mechanisms fail.

Did you know…In the 1976 Montreal Olympics, the gymnastics electronic scoreboard could only display three digits, which meant that when Nadia Comăneci unexpectedly scored the highest possible perfect 10.00 score, the scoreboard instead displayed a lowly 1.00. |

As previously mentioned, expert determinations are binding on the parties, making them a strong option to reach a full and final resolution. They are not open to challenge or any appeal processes, except in very strict circumstances, where it can be proven that the determination is incorrect due to either fraud or manifest error.

Did you know…Tug of war was contested at every Olympics from 1900 to 1920, with Great Britain being the most successful nation, winning two golds, two silvers and one bronze. |

Our Forensic Services team have extensive experience of being both the expert determiner as well as assisting parties in preparing their submissions to the appointed expert determiner. For more information, please contact Martin Chapman or your usual Crowe contact.

Did you know…In the 1936 Berlin Olympics two Japanese athlete, Shuhei Nishida and Sueo Ōe, cleared the same height in the pole vault, being awarded silver and bronze. Being good friends, they had their medals cut in half, and fused into two hybrid half silver and half bronze medals, which became known as “The Medals of Friendship”. |

In cases where one side is aiming to make a claim — be it for loss of profits, breach of warranty, professional negligence, or similar — it can often be the case that such a claim may be overstated or exaggerated in some way, sometimes artificially and sometimes simply through an incorrect approach to formulating the claim.

For more information on the services we offer, please contact Martin Chapman.

Did you know…A poorly formulated, or incorrect claim, can cost a company significant management time, as well as incurring wasted Court costs. |

As forensic accountants, our involvement in the buying and selling of companies is usually required when something has gone wrong and there is a completion accounts dispute, earn-out accounts dispute or warranty claim. Disagreements in the interpretation of share purchase agreements (SPAs) can be the root cause of the disputed matters. Below we set out some real world examples, that based upon our experience, are best avoided.

We have been involved in matters where warranties have been agreed along the lines of company forecasts being ‘carefully’ prepared, or specific clauses inserted requiring ‘appropriate’ provisions for liabilities to be made.

Ambiguous terms such as these are unhelpful, as each party will undoubtedly have different interpretations as to what ‘carefully’ or ‘appropriate’ means in practice. Leaving room for the application of judgment in accounting practices can lead to vastly different conclusions as to the consideration due under an SPA.

Unrealistic warranties

A warranty we often see proposed at the SPA drafting stage, but thankfully is usually (but not always) removed in the final SPA is that “the management accounts have been prepared in accordance with Generally Accepted Accounting Principles (GAAP)”.

GAAP in the UK is typically FRS102 or IFRS , being the principals dictating how companies produce their annual statutory financial statements. Management accounts, while often having a significant grounding in GAAP in their preparation, are produced internally by a company to assist management in running the business. Differing reported financial performance can arise, for example, when management accounts use interim estimates, instead of detailed calculations that would be required under GAAP.

Having a clause in an SPA that warrants that the management accounts have been prepared in accordance with GAAP likely leaves a seller open to a warranty claim, because management accounts are very rarely, if ever, prepared completely in accordance with GAAP.

SPAs typically have a hierarchy set out, that dictates how completion accounts and earn-out accounts are prepared. The most common hierarchy is:

We have seen examples where the wording as to the hierarchy applicable is unclear, which can result in buyers and sellers having vastly differing opinions as to how completion accounts or earn-out accounts should be prepared and ultimately the resulting consideration due.

SPAs go through numerous different versions during the drafting process. It can be very unhelpful if a clause in an SPA, refers a different clause in the same SPA, but does not reference the correct clause number, or is referencing a clause that no longer exists, owing to drafting revisions.

In worst-case scenarios, this can make clauses have completely different, unintended meanings, resulting in buyers or sellers being unfairly financially worse off in terms of the consideration ultimately paid.

Problems can arise if SPAs are silent in respect of defining a cut-off date for the admissibility of evidence for consideration, when preparing completion or earn-out accounts.

An example where a cut-off date could have a big impact on consideration due would be the parties becoming aware, after the completion or earn out accounts date, that a key customer, owing significant monies, has gone into administration. Without a defined evidence cut-off date in the SPA, disputes could arise as to whether it is correct to write-off these amounts owed in the completion or earn out accounts.

Our experienced Forensic Services Team can assist advising, or acting as an accounting expert witness, for buyers and sellers in respect of completion account, earn-out account and warranty disputes. We can also perform the role of expert in expert determination processes (see our Top 10 tips for a successful expert determination article from earlier in the year).

For further information on our forensics services and how we can help you, please contact Martin Chapman.

Did you know…According to the Office for National Statistics, in the twelve months to 30 September 2023, 1,134 UK companies with a value of £1 million or more were acquired, 851 being acquired by other UK companies and 283 being acquired by foreign companies. |

Let’s start with the ‘fairy-tale’ scenario (a particularly appropriate phrase in the context of this article, as will become clear) that the parties are in complete agreement with the £100 million company value concluded by the forensic accounting expert, in which one of the parties holds a 20% shareholding.

At first glance, you would think 20% of £100 million; the shareholding is worth £20 million (applying a simple pro-rata calculation), but that may not be the case. Often, a ‘minority discount’ would be applied to this £20 million, to reflect that the 20% does not give the shareholder control of the company and the decisions made with regards to, for example, its strategy, investment decisions or its use of profits.

Depending on the circumstances, minority discounts can typically wipe out up to 75% of the pro rata value and this percentage can sometimes be even higher. In the context of this £20 million example, a 75% minority discount reduces the shareholding value to £5 million, so the legal arguments put forward as to whether a minority discount is applicable can make a huge difference.

Majority of the time, for this 20% shareholding to be worth the full £20 million, a judge would have to conclude that the company is a “quasi-partnership”, but in what circumstances can this conclusion be reached…

Take, for example, the Three Little Pigs and their renowned architectural design empire. Ignoring for a second the multiple accusations of health and safety breaches in the press (apparently straw isn’t a safe building material), using case law from RM & TM [2020] EWFC 41, a judge may conclude that a “quasi-partnership” is in effect:

“These are family businesses. The family is likely to act in concert on major decisions, such as sale…Their personal relationships are strong, with no evidence of major internal disputes or quarrels…This, in my judgement, bears all of the hallmarks of a quasi-partnership and I therefore will not attribute a valuation discount.”

A judge may reach a “quasi-partnership” conclusion in respect of The Seven Dwarfs and their international network of diamond mines. Case law from FRB and DCA [No 2] BV17D16308 [2020] is particularly apt given the dwarfs’ insular operations as a reaction to havoc caused when they temporarily let a certain Ms Snow White into their tight-knit organisation several years prior:

“This is the perfect example of a quasi-partnership to which a discount will not attach. I accept that if an outsider were to buy into one of these companies, he or she would expect a discount, but it is in my judgement inconceivable that any outsider would either be permitted ownership or be interested in acquiring it.”

Finally, we highlight the ‘Bag a Royal’ dating app that is taking the world by storm, the latest in a long line of apps published by the well-known behemoths of software development, Cinderella, and the Fairy Godmother. Clarke and Clarke [2022] EWHC 2698 (Fam) would likely be cited in favour of a “quasi-partnership” in respect of this business:

In his oral evidence Mr Clarke stated that he has been trading with his partner, Mr Shadforth, for many years and he would imagine that they would always take decisions jointly.”

As forensic accountants, our fully CPR Part 35 / FDR Part 25 compliant or advisory reports set out company valuations in simple and understandable language, showing both the pro-rata and minority discounted valuation of shareholdings as required. It is the responsibility of the parties’ solicitors to make their respective legal arguments as to whether a “quasi-partnership” is in effect, although we may be asked our opinion on accounting matters that might contribute to the conclusion as to whether there is a “quasi-partnership”.

For further information on our forensics services and how we can help you, please contact Martin Chapman.

Did you know…The largest known divorce settlement in the UK is £554 million, being that ordered to be paid by Sheikh Mohammed bin Rashid Al Maktoum to Princess Haya bint al-Hussein in December 2021. |

A vital first stage of accepting any instruction is to ensure that you are not compromised in your position whereby you must be, and be seen to be, independent. As such, there should not be any material relationship with the parties involved in the dispute that could create a scenario, whereby it appears you have reason to favour one side or the other. A typical scenario that might exclude you from acting on a matter is where your firm act as auditors for one of the parties, or you are personally connected in some way, in either a current or previous business relationship.

The principal way of checking that you are conflict free is to contact the partners of the firm, and should there be any overseas parties involved, a check will also be extended to overseas network offices. An internal check of your own firm’s database of contacts also helps establish that no conflicts exist.

Alongside this, there are certain cases that may need high level clearance from the firm - normally authorised by a small number of partners and senior management nominated to oversee the process – this would cover cases that might be seen as having a public interest perspective, relate to individuals or countries connected with political or civil unrest and/or the level of fees or amount in dispute makes heightens the risk of accepting the appointment. In these instances, the approval committee’s role is to safeguard the reputation of the firm and consider whether the proposed assignment should be undertaken.

Instructions provided to the expert witness would usually include the scope of work being requested (i.e. the work that is to be delivered), how that will be delivered (most commonly through an expert report compliant with either Part 35 of the Civil Procedure Rules, Part 25 of the Family Procedure Rules or Part 19 of the Criminal Procedure Rules) and will typically include the background to the case and a set of guidelines for reporting experts. It may also, at that stage, set out the court timetable, specifically when the report needs to be filed by, and may additionally include the deadline for any joint meetings and statements with the expert on the other side.

In response, an expert would issue their own terms of engagement which is the contract between them and the instructing party that forms the legal basis under which they will act as expert witness. This sets out which members of the team will work on the case and what their hourly charge out rates will be – where possible, a fixed cost of carrying out the work will be provided or, if the volume of work to be conducted is unclear or subject to variation, the terms might allow for charges to be made on a time basis based on those hourly rates.

The other essential element to an expert’s instructions are the timelines - when their report needs to be filed into court, and the various stages of review along the way that are agreed with the instructing party and may be set out in the terms of engagement.

Terms of engagement will also contain the general terms and conditions of business that apply to that expert’s firm, for any of the services it undertakes as a business and form an important legal part of the overall engagement, providing a safeguard for the commercial interests of the firm. This will also include a clause around the limitation of liability that the firm accepts in respect of the engagement.

Should any dispute take place at a later date – about the nature, scope or cost of the work undertaken - it will be the firm’s engagement terms that will act as evidence and, in that respect, their importance must never be underestimated or compromised.

For further information on our forensics services, and how we can help you, please contact Martin Chapman or your usual Crowe contact for more information.

Did you know…It is always worth knowing other expert witnesses to recommend should any issues arise that prevent your firm accepting instructions to act on a case. |

Investigation and consideration

The substance of our work will involve some form of investigation, research, or analysis, with evidence obtained by reviewing a company or individual’s’ accounting records. Incomplete records might typically require further investigation and explanation.

Information from third parties such as banks, customers and suppliers can be useful third party, independent evidence, which can be reviewed to corroborate information seen elsewhere. Further information and documentation may be sourced from the public domain.

Expert report

An expert report flows from our substantive work, in which a reporting partner will express a formal opinion. The report must comply with the strict requirements set out in the Civil Procedure Rules (CPR) and will ultimately be disclosed, should a settlement not be reached before trial. It’s vital the report be written from an independent and non-partisan perspective, with the ultimate objective being to assist the court.

Conclusions and opinions should be robust and supported by evidence, able to withstand cross-examination and critical analysis.

Meeting with the other side

Where an expert is appointed by each side, a meeting of experts might typically be held, and a joint statement prepared to assist the court.

This joint statement summarises areas where the two experts agree, and disagree, providing further analysis where relevant.

Pre-trial support and attending trial

Pre-trial support might include a conference with counsel, and assistance at mediation, while a trial might see the expert supporting the litigation process at court, by giving evidence in person. A forensic accountant can recommend areas of cross-examination to their side’s barrister, on the accounting evidence and can equally be cross-examined on their own work. The expert’s fundamental responsibility is to the court, and not his instructing solicitors.

As highlighted above, commercial disputes can be a complex process. At Crowe, we have an experienced team of forensic accountants who can provide support at every stage of the process, and provide clear, concise advice.

Did you know…There are standard paragraphs which must be included in an expert witness report and templates for these can be found on The Academy of Experts website. |

To explore the challenges forensic accountants, encounter when it comes to quantifying such claims, below I consider the recent plight of Livchester United, the most successful ‘fictitious’ football team in Europe.

Despite being in the north-west of England, famous for its low rainfall, three years ago Livchester’s Oldfield stadium suffered a catastrophic flood, making Oldfield uninhabitable for a year whilst repairs were made. Thankfully, the club had insurance which covered not only the cost of repair but also facilitated a business interruption claim under the Act of God clauses.

The forensic accounting expert had a straightforward claim to quantify (albeit, evidencing and justifying such claims can sometimes be a challenge) and was able to assess Livchester’s lost profit by:

Having begrudgingly spent a year playing at The Goodihad, Livchester were outraged to find out that their Messaldo Stand (the main spectator stand at Oldfield, named after the club legend and the undisputed greatest player of all time), would not be ready for the contracted repair completion date. Livchester had to spend a further year operating with their ground capacity at only 70% of its maximum.

Again, the forensic accountant was on hand to quantify a business interruption claim, this time against the building contractor that had failed to complete the repairs on time. Whilst conceptually, the quantification was a similar approach as prior, comparing actual profits to a ‘but for the contract breach’ scenario, there were several complex circumstances the forensic accountant had to factor into their calculations:

As if that was not enough, the day after the Messaldo Stand reopened, Livchester received a CPO on Oldfield, as part of the UK Governments HS10 plan to provide the public with high-speed travel to Lands’ End. They had to relocate and rebuild a new stadium fifty miles away, which was very upsetting for the club and its fanbase, with the only silver lining being that Livchester received significant compensation from the UK Government for losing Oldfield as well as being entitled to the loss of profits from the resulting business interruption.

The complexity of the forensic accountant’s work increased further, having to consider similar issues to before, but also this time factoring in ongoing losses into the future. Livchester’s new stadium had a significantly smaller capacity (losing gate and hospitality receipts) and it lost some of its fanbase due to the geographical move, both of which limited how lucrative future sponsorship contracts would be.

As highlighted in the above scenarios, assessing the quantum in a business interruption case can involve factoring in several complex hypothetical assumptions. As forensic accountants we are used to simplifying complexity, setting out reasoned logical and evidenced opinions and conclusions in a simple and straightforward manner.

For further information on our forensics services and how we can help you, please contact Martin Chapman

Did you know…The Association of British Insurers estimated COVID-19 business interruption claims in 2020 to be circa £2 billion. |

Many notes are required under accounting rules, while some may be disclosed at the discretion of the directors, although a common approach (of private companies, listed company rules are more onerous) is often to disclose less rather than more. Some of the notes that an expert will have an interest in, whether it be for the purposes of a valuation or a loss or profits calculation, include (but are not limited to) some of the following areas.

This forms a key part of valuations, with an analysis usually forming part of most experts’ reviews, with a view to assessing whether these payments have been made at market rate or may need adjusting to reflect the true cost to any purchaser of the business – total remuneration is normally disclosed along with what the highest director has been paid – bear in mind a director’s remuneration package might include not only base salary but also bonuses, medical and car benefits, and pension scheme options.

Disclosure often needs to be made around which transactions have been conducted with parties who are related and potentially not at arms’ length (i.e. not a sum that would be paid to / received from unrelated third parties), again potentially requiring adjustment in any analysis – a common adjustment is rent payable to a related party that might be understated and not at market rate.

Creditors less than and more than one year, relating to bank loans, will be shown in the notes and is an important part of assessing the debt a company has to service and whether that business relies on its own resources to support its working capital requirements or is more reliant on external funding.

Normally towards the very back of the notes will be disclosure around who the ultimate parent company is that controls the company, it may be the case that this company is the sole subsidiary of a non-trading holding company, or conversely could be one of many subsidiaries held by a large trading parent company with a wide portfolio of operations.

Accounts are drawn up at a specific point in time, such as 31 March, 31 December etc and include the transactions, and year end balances, for that period (resulting in profit or loss, net assets or net liabilities) including the company’s balance sheet which is a snapshot of its financial position at a particular point in time. However, the accounts for a business are prepared after the period has ended and therefore, between the date of the accounts and the date they are signed off, certain events may take place that need to be disclosed, either because they provide further information about something that occurred during the period, or they represent a fundamental change in the nature, assets or debt of the business that merits reporting. Such an occurrence may be something like the sale (or purchase) of a business in, say July, when the company’s year end was March.

At the start of the accounting notes will be a summary of the accounting policies adopted by the company – certain accounting standards allow an option (e.g. an asset depreciated on a straight line or reducing balance method) and this can have a material impact on the profits recorded by the business, therefore a good understanding of which accounting policies are applied may help in any analysis of that business. This may be particularly relevant to items such as revenue recognition, or businesses that operate long-term contracts.

Many companies will disclose provisions, these are typically the Directors’ assessment of future payments due that are currently quantifiable (but not yet payable), and such a provision may be made in the accounts – such items may include provision for a potential tax charge, the costs of legal action, or non-payment of a material debt – certain provisions might be classified as a ‘contingent’ liability i.e. the profit and loss account won’t be impacted for the period but the nature and/or size of the matter is of such significance that disclosure is made in the notes.

For further information on our forensics services and how we can help you, please contact Paul Burchett.

Did you know…Private companies have nine months to file their accounts following their year end (although special provisions were in place during the COVID pandemic that extended this by a further three months). |

Untangling the knots between two parties at the end of a marriage can be a painful and complicated process. The recent high-profile case, Standish v Standish, has thrown the spotlight on this issue, in the context of matrimonial and non-matrimonial assets, with the importance of the source of wealth being a key battleground between the Parties, as the matter has passed through the High Court, Court of Appeal and UK Supreme Court.

The following fictitious divorce case between Jack and Jill, highlights how different assets and arguments might result in vastly different decisions by the Court, when distributing their wealth.

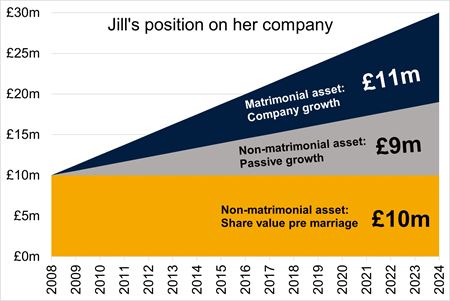

Jack, being the more eccentric of the parties, owned a 24-carat, bejewelled, solid gold crown (which ironically was once broken during an incident where he and Jill, his then fiancé, fell down a hill). It was straight forward for the Court to determine that this was a non-matrimonial asset to be retained by Jack, as he owned it before the marriage, with the crown just sitting in the attic amongst his equally flamboyant vintage waist coat collection during the course of the marriage. Jack was particularly relieved about this given that the crown had risen in value from £10 million at marriage to £30 million at divorce, thanks to the vast increase in the price of gold bullion since 2008.

Jill’s situation was more complicated however, as an asset she owned was shares in a bottled spring water company, of which she was the Managing Director (again ironically, the springs’ source is at the top of the hill that Jack and Jill took a tumble down, when the aforementioned crown was broken). Coincidently, the value of her shares in the company had also risen from £10 million at marriage to £30 million at divorce.

Jack argued that all of the growth in the company value since marriage (i.e. £20 million) should be shared equally between the parties, as Jill was only able to build up the company due to their joint, but inevitably different, efforts during their marriage. Jill thought this was incredibly unfair, particularly given the converse position with Jack’s crown where he massively benefited from the passive growth in gold bullion prices without any effort on his part.

Jill argued that some of the growth in the value of the bottled spring water company had happened passively without her efforts. She cited the trend of the increase in value of companies on the London Stock Exchange as evidence that companies are subject to passive growth, in the same way that commodities such as gold bullion are.

Jill calculated that had her company’s value grown inline with London Stock Exchange companies since the marriage, at divorce it would have been worth approximately £19 million; passive growth of £9 million since the £10 million valuation at marriage. Jill’s proposed that only £11 million of her company’s value was a matrimonial asset for sharing between the parties (£30 million company value, less £9 million passive growth, less £10 million pre marriage value).

As the below illustrations demonstrate, the contrasting positions held by the parties in respect of the bottled spring water company, could result in vastly different conclusions as to the value of the ‘matrimonial pot’ to be shared. The opinion of forensic accounting experts could be key to swaying the Court’s verdict on this.

As well as providing the ‘usual’ forensic accounting expert witness services in respect of matrimonial matters, such as valuing shares, considering capital extraction from businesses and the corresponding tax implications, we are also comfortable dealing with niche areas that can pop up from time to time, such as passive growth, be that as a single joint expert, party expert or shadow expert.

As an expert witness, the preparation of a report is an important process to assist the Court by summarising findings within your area of expertise. Here are 10 top tips for preparing a good expert witness report.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…The Academy of Experts offers training, including a foundation course which includes report writing. Details of the courses offered can be found here. |

Intellectual property infringements are one of the instances where, as forensic accounting experts, we usually don’t get involved until after liability has already been proven. We are brought into the case knowing there is going to be some kind of award for damages, it’s just a matter of determining how much.

This article examines two of the possible routes that can be taken when quantifying losses, and has been written following a recent case in which Martin Chapman aided his client in receiving a landmark £13.4 million intellectual property infringement damage award, and £900,000 by way of costs (Geofabrics Ltd v Fiberweb Geosynthetics Ltd [2022]1).

Disclaimer: A fictitious case study is used below to demonstrate the possible proceedings following an incident of intellectual property infringement.

We address the case of Rugs Undermining Gravity Limited (“RUG”), a wholesaler of magical flying carpets, having its premier product the FlyRUG, infringed by Making Amazing Threads Limited (“MAT”).

n.b. There is a third option available not covered in this article, involving the claiming of royalties.

RUG’s objective is to maximise the damages awarded to them, so what should they do?

This requires RUG to estimate the additional profits they would have achieved, had the SoarMAT not been available (the “But-for Scenario”). This is where the forensic accountants will come to the fore as they will be able to quantify this, considering for example:

While inherently complex, this approach has a key benefit for RUG, in that it is the owner of most of the information needed to compile its claim and thus is more able to influence the quantum.

This approach might be used where, for example, MAT is a much bigger brand than RUG and was able to achieve much higher profits than RUG would have been capable of under the but for scenario.

The forensic accountants will be helpful in quantifying these profits, as complex assumptions are involved when assessing which costs (or proportions of costs), are actually attributable to SoarMAT sales. Company overhead apportionment is often a significant battle ground here.

This option can be more straight forward as is based upon what actually happened, rather than the but-for scenario. However, RUG has the disadvantage of not being the owner of the information needed, and is thus reliant on MAT making adequate and accurate financial disclosures. RUG’s forensic accountant can assist in identifying any areas of disclosure that are lacking and critiquing the account of profits presented by MAT, offering their own opinion on quantum.

We have a team of experienced Forensic Accounting Experts who are equally comfortable acting for claimant or defendant, providing expert reports and testimony to the Courts. If you would like more information on our services, please get in touch with Martin Chapman.

Did you know…According to an article 2 published by Wolters Kluwer, between 2000 and 2019 there were only four UK patent cases in which damages awards were made by the UK Courts, totalling about €1.6 million. This puts into context the magnitude of the recent £13.4 million award to Geofrabrics Ltd. |

1 https://www.bailii.org/ew/cases/EWHC/Patents/2022/2363.html

2Article published on the Kluwer Patent Blog, dated 13 September 2021, entitled "The Hit Parade of Patent Infringement Damages in Europe: France is Great (Again)" by Matthieu Dhenne, available at: http://patentblog.kluweriplaw.com/2021/09/13/the-hit-parade-of-patent-infringement-damages-in-europe-france-is-great-again/

As an expert witness it is important to demonstrate certain qualities, to assist the Court in making their judgment and to safeguard the reputation of both yourself and your firm. Below is by no means an exhaustive list but includes some of the more important qualities.

An expert witness’s overriding duty is to the Court and not the person instructing them or discharging their fees – independence, impartiality and integrity must be maintained notwithstanding any pressure that may come from solicitors, barristers or lay clients to influence your opinion or how the case may be presented.

A Court will not look kindly upon any expert that changes their mind all too conveniently, or one that professes a certain approach in one case but then changes that drastically in another matter – if new evidence has arisen a Court will always accept that your opinion may have changed but someone who changes their opinion without due cause will have their credibility quickly undermined.

A Court will give more credit to an expert that has considered the facts and evidence of the case without any bias towards his client – one method adopted by many experts is to produce a range of outcomes where the information available to them is not strictly ‘black and white’, providing alternate conclusions based on alternative assumptions. Credit will also be given where the expert accepts and amends their opinion where valid points are made.

An expert who puts his name to a report must be mindful that the views and opinions expressed within that report are theirs, and theirs alone – a highly qualified, efficient support team may have assisted in drafting a high quality report but if the expert has not had sufficient input, or gained a detailed understanding on the matter, then their credibility could very quickly be attacked under cross examination.

Give the Court what they need – your accounting input set out in a fashion that sets out the key points, avoids confusing terminology or over complicated calculations, and ‘tells the story’ of what has happened, your opinion, and the key accounting points the Court needs to consider in making its judgement. A Court that doesn’t have to struggle to work out what you have written, and what your opinion is, may assist in seeing your evidence ultimately being favoured.

Behind every expert is invariably a hard-working team that supports the drafting of the report – ideally the expert will have a team that has a good blend of experience and specialist knowledge that they can draw upon to present the accounting evidence.

Underlying everything that is produced by the expert witness lies the importance of quality, both from the correct use of basic grammar all the way through to the final opinion you provide. Not only will this assist the Court and reinforce your position as a professional that can be trusted, but it will also see instructing parties refer further work to you.

It is important that an expert witness delivers their work to the timelines set by the Court, which includes ensuring sufficient time is set aside for discussions with instructing solicitors and work is appropriately allocated to members of the expert’s team.

If you work in a practice that has overseas offices, the option and benefit of having other colleagues from around the globe can assist on cross jurisdiction matters.

Finally, a useful quality for any expert witness is to know other experts that cases can be referred to, should the case they have been asked to act on has a conflict to prevent them from acting, or requires a particular specialism which is more suited to another expert.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…Expert witnesses can be subject to personal criticism in judgments made by the Court should the qualities they display fall below the standards expected. |

It is of vital importance, whenever considering making a financial claim in a legal matter, that relevant and sufficient accounting evidence is produced to support that claim.

We have recently been involved in a case where the Claimant was seeking to recover damages from former directors of a Company that had been placed into liquidation. There were allegations that the former directors had under declared takings, and retained these personally, rather than recording them within the Company’s accounting records.

HMRC had previously investigated the Company and, at one point, its former advisers had sought to negotiate a settlement of the potential tax liability. The Claimant sought to use this correspondence as its primary evidence to prove that such under declaration of takings had taken place, and consequently the directors should be held to account for this amount of money.

We were instructed by solicitors representing two of the directors, to provide forensic advice, and undertook various exercises to assess whether there was any evidence that there had been an under declaration of takings. The records available to us, however, were very poor and broad brush assumptions had to be made.

This involved a critique of the business economics exercise HMRC had undertaken to create their original estimate of the level of under declaration. Key features included the amount of wastage in the sector and the level of customer complaints and credits/non payment of debts.

The Claimant decided not to adduce expert evidence in relation to demonstrating the alleged under declaration of takings, and proceeded to trial solely on the basis of the documentary evidence they had obtained.

At the Pre-Trial Review, the Judge expressed surprised at the lack of forensic accounting evidence, and, at the hearing, attempted to recreate his best assessment of what appeared to have taken place. It was gratifying to note that the thrust of his analysis mirrored that which we had previously prepared.

In summary, the Judge found that the Claimant had not discharged the burden of proof to establish that their allegations were properly made out, and awarded significant costs against them.

This case demonstrates the importance of assessing what evidence is required to be collated or adduced, in order to demonstrate that a claim has been properly set out, otherwise the consequences can be both costly and damaging.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…It is often of benefit to approach a forensic accountant early in a case to identify how best to demonstrate the losses arising. |

Back in the day the expression “hired gun” was sometimes levelled at certain expert witnesses (and not just accountants) implying that they were singing to their instructing solicitor’s tune. However, moving into the 21st century and that expression has now thankfully fallen out of parlance. We as forensic accountants, in our role as an expert witness, recognise our duty and responsibilities are to the Court, and not the person instructing us or settling our fees. This can lead to tensions between us and the legal team in terms of their roles as advocates, and us as independent reporting accountants.

But ultimately, when litigation is in full swing, independence is at the heart of all the work we do and reinforces our credibility, being seen as the product of our own opinion based on the financial evidence gathered.

It does, of course, mean taking a strong stance if Counsel or instructing solicitors want you to adopt a particular approach which does not reflect your opinion. Being resilient is vital, both for your own reputation as an expert witness, and also for the legal team and their client, as independent evidence will gain more credibility from the Court than reports that are seen to be unfairly weighted towards the client. There have been several cases in recent years where we have been initially asked to discuss the merits of a claim, very sizeable in many cases, where our independence has led to advice that there is not a claim that can be properly supported, or that the claim as presented is nowhere near as large as initially considered.

Our independence is always checked at the outset through conducting conflict checks to ensure no accusation of bias, or “marking your own homework” can be levelled. For instance, if you are reviewing the accounts of a company that your firm has audited for many years, or reviewing the performance of a company one of your partners may have an interest in, or similar.

Ultimately, the Court wants an Expert Witness to assist the Court by providing a report that makes technical accounting jargon, or rules, easy to understand, provides the Judge with relevant information upon which to base their ruling, and for the report be unhindered unduly by the influence of the clients’ advocates or the parties contesting the litigation. Our duty is to assist the Court, be independent and be seen to be independent, serving as an aide to the Court rather than produce further conflict or confusion.

We can help in relation to expert determination proceedings, and have considerable experience both as advisers to the parties, and of acting as the expert determining the dispute. If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…That an Expert Witness’s duty, and responsibility, is to the Court and not the entity instructing or paying them. |

Expert determination is a procedure that involves a dispute, or difference, between two parties which are submitted to one or more experts who make a determination on the matter presented to them. The opinion reached is then binding on the parties, unless they both agree otherwise.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…An expert determination is usually quicker, cheaper and less formal than arbitration or litigation. |

Forensic accountants are often instructed on professional negligence disputes.

In professional negligence cases the defendant may be a firm of solicitors, accountants, or architects that have previously provided some form of advice or work which is now alleged to have been below the standard expected, causing a financial loss.

The claimant must prove three areas:

The latter is a crucial part in any professional negligence claim as unless a direct correlation can be made between the negligent advice/work and any resulting loss, a Court is unlikely to find in favour of the claimant.

There are two broad alternate aspects to any work we undertake – firstly reviewing the work undertaken by an accounting professional to identify whether it has been performed in an acceptable manner, or secondly reviewing the claim on the assumption that work was negligent but being instructed to assess any loss arising.

The test for professional negligence (e.g. an accountant) is fundamentally what you would expect a reasonably competent accountant to have done based on the accounting and auditing standards, generally accepted accounting principles, and practices that were in place at that time. It is not the case that you are giving an opinion on what you would have done at the time but rather, from your experience of conducting similar work and familiarity with other accountants’ work, whether you consider the defendant has carried out their work to a reasonable standard.

As the expert witness must have relevant contemporaneous experience, our forensic team will frequently work alongside experts from other disciplines within our firm to provide a seamless service.

In terms of any resulting award made by the Court, the defendant professional will usually carry insurance against such claims being brought against them and that insurance company will make the funding decision as to the appointment of an expert witness to prepare a report, based upon advice provided by the defendant’s solicitors. The financial consequences of a claim will depend upon the impact on the claimant’s business, but will frequently be assessed in the same manner as a loss of profit or business interruption claim.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…Professional negligence is when a professional fails to perform their responsibilities to the required standard or breaches a duty of care, which results in financial loss, physical damage, or injury to a client / customer. |

There are various traits that are important to possess to enable you to represent your client in expert witness work. More importantly, the skillset is needed to deliver your prime responsibilities to the court, and ultimately lead to a fair assessment upon which the Court can make their judicial decision.

In years gone by, there was an overwhelming feeling - that ultimately led to reform - that experts were often regarded by those instructing them as ‘hired guns’, making the evidence fit the conclusion that would best assist their clients.

Our overriding duty is to the Court, and not the party instructing or paying us. Ultimately, we must maintain our independence notwithstanding any pressures exerted either from solicitors or lay clients. There have been various cases we have been instructed on where we have had to tell our solicitors – “sorry, but your case can’t be supported on the evidence available”, this is not what the solicitors or client may necessarily want to hear but to avoid such a conversation would be to undermine your own opinion and work.

At times solicitors may try and put some gentle pressure to change an opinion, or a working, but if you are clear that what you have concluded is (to your mind) correct, then your professional duty is to remain resolute.

Another quality required is consistency – a Court will not take kindly to an expert changing his mind with the wind, or worse still, expressing one opinion on a specific matter in one case, then at some point later addressing essentially the same matter but adopting a completely contradictory approach (with no good reason to do so). A Court will always accept if you have had access to new evidence which has impacted your opinion, but someone who is willing to change their opinion so easily is not a robust expert witness whose evidence will be accepted by the Judge.

Further, an element of fairness to any report, or verbal evidence given in Court, is key in supporting a crafted argument – if a report is totally weighted towards one’s own client throughout then it can bring into question the independence of the expert. One useful method adopted by many experts is the adoption of a range of conclusions, particularly when there is a monetary aspect, to give the Court an idea of what range the claim may lie within. This may be couched within terms such as if we assume ‘A’ the claim is £Y, but if we assume ‘B’ then £Z may be more appropriate.

An area in which an expert giving evidence at Court can undermine his own case is where the report may be absolutely fine, in fact it may be one of the best reports ever produced. But if that expert has overly relied on his team to prepare the report, and the understanding of its methodology and underlying assumptions is not fully understood or concluded by the expert, then the expert’s evidence will be quickly undermined under cross examination and a perfectly good report potentially made redundant.

It also helps an expert to be a good story teller – not making things up of course – but delivering a report that takes the reader (and the Judge) on a journey, where the issue is set out, and signposts set early on in the report for what is coming later. There is nothing worse for a judge than to have read a report and by the end be completely lost or confused as to what they have had actually just been told – wherever possible, the simpler and less technical the language, the better.

If you would like more information on our expert witness service please contact Martin Chapman.

Did you know…The Academy of Experts help you find a qualified expert witness to assist you on your case and also provide training courses for those who act as expert witnesses. |

One area where we often provide expert support is in the form of Expert Determinations (ED). ED is a procedure which involves a dispute, or difference, between two parties which are submitted to one or more experts who make a determination on the matter presented to it or them. The opinion reached is then binding on the parties, unless they both agree otherwise.

An ED can be beneficial to the disputing parties as it is less costly than going to Court, a faster process, is usually binding on the parties, and is subject to the opinion of an independent accountant who has no allegiance to either side.

The resulting opinion can take one of two forms – non-speaking or speaking. There are pros and cons associated with each. A non-speaking approach is exactly as it sounds, say a company valuation is being undertaken, the non-speaking opinion will state is that ‘the shares are worth £X’. There are no report details to be challenged and as such it is difficult to challenge the outcome, although one side will invariably be happier with the outcome than the other.

A speaking valuation is the opposite of a non-speaking valuation and will set out in detail how the value for those shares has been reached in a format more akin to a traditional report disclosed for Court. It has the benefit of covering the issues that may have been in debate between the parties, explaining why the conclusions have been reached. A speaking valuation may also raise matters which the parties wish to challenge that could end up protracting the process (for instance if they think something is factually incorrect). The threshold for challenging a determination on its findings is high, however, as the test is normally whether there has been manifest error.

We can be instructed either as the expert undertaking the determination or assisting one of the parties in preparing their submissions. If you would like more information on our expert witness service please contact Martin Chapman.

In simple terms, we are the numbers support service to litigious disputes, investigations or advisory work and are frequently instructed to prepare reports for Court on what can be very complex, or hotly disputed, accounting/number issues. Sometimes our work can be conducted on an urgent basis within a day, but often the work continues over many months, or even years. Although our clients will always want the best outcome for themselves, our responsibility as an expert witness is to the Court while if we acts as advisors we will present both the strong and weak points of a client’s case, possibly ahead of mediation or consideration of a legal claim. Our work can take us anywhere within the UK, and across any industry, while we also take on overseas matters due to our well established Crowe Global network of over 750 offices across 130 countries.

Our work is not supported by a portfolio of clients like it might be in audit or tax service line, each year a different set of challenges and scenarios is presented to us as we seek to assist our clients in either their dispute, investigation, or analysis. While not professing to be the ultimate experts in every field of industry, we need to be sufficiently capable of being able to quickly pick up how various businesses operate, and what are the real issues that will drive the case either at Court, mediation, or in other negotiations. While we always want to help our clients it is also important that we maintain an independent thought process which sets out the respective merits of a case, both good and bad from our client’s perspective.

The matters we work on are often diverse and regularly challenging, examples of the range of casework we have been instructed on include:

If you would like more information on our expert witness service please contact Martin Chapman.

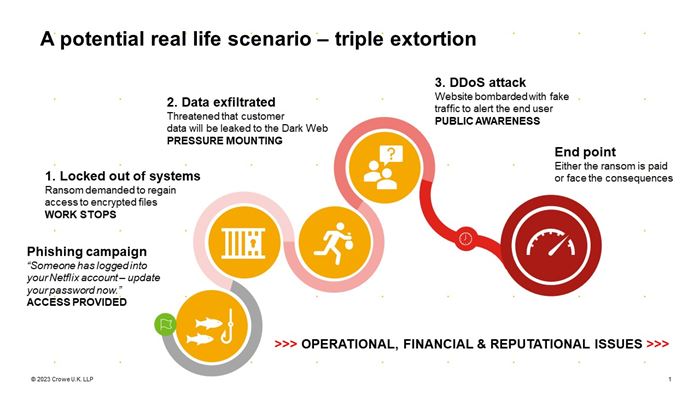

Most organisations are aware when they have been hit by a cyber attack. However, this awareness often does not extend to Advanced Persistent Threats (APTs). While your organisation's systems and networks may seem perfectly fine on the surface, hidden dangers could be lurking beneath.

APTs are sophisticated cyber attacks conducted by threat actors over an extended period, where they breach a network and maintain undetected access to information. By leveraging social engineering tactics, adaptive malware, and exploiting trusted systems, APTs can evade traditional cybersecurity measures. The longer an APT remains undetected, the greater the potential for financial, operational, and reputational damage to the organisation.

In 2024, one in four companies were the target of an APT, increasing by 74% compared to 2023. Additionally, around 50% of cyberattacks on supply chains were attributed to APT groups. Any industry can be a target of an APT, but organisations in the finance, healthcare, IT, and governmental sectors are predominantly targeted due to the sensitive information they hold.

Unlike most cyber attacks, APTs are not intended to cause immediate damage, but to acquire and maintain continuous access to sensitive information. APT attacks are conducted in stages.

While it is challenging to notice its presence within your system or network, below are some indicators of a potential APT attack.

Our Forensic Services team provide a range of services to help your organisation mitigate vulnerabilities and reduce the risk of attack. For more information on the services we offer, please contact Tim Robinson or your usual Crowe contact.

Did you know…Investment in APT protection is projected to reach USD 20 billion by 2027, representing a 365% increase since 2019. |

To those initially starting a business, it may seem that small start-up companies would not be an appealing target to cybercriminals. However, cybercriminals are targeting smaller companies as a gateway to larger organisations they may work and/or interact with.

Smaller companies are less likely to have considered cybercrime as a risk, and thus are less equipped when it comes to having security measures in place to detect, prevent and protect itself against potential cyber incidents. It is easier for a cybercriminal to infiltrate a smaller companies’ systems and networks, than it is with a larger organisation that will have a dedicated cyber security team, has extensive measures in place, and maintains certification to regulatory industry standards such as ISO 27001 and SOC 2.

The threat can be both internal and external.

The biggest internal threat is human error. While it is the intentions of some employees to inflict a cyber related incident, the majority of the time it is purely accidental. Research has found that 95% of cyber data breaches are caused by user error. Unsafe practices, and employee unawareness of cyber and information security threats, can leave an organisation – and its assets – vulnerable to cybercriminals. One of the most common examples is an employee accidentally clicking on and downloading a malicious file that then infiltrates an organisation’s internal network with malware.

In addition, external threats can put a company at risk on a regular basis, with statistics showing that 31% of businesses are targeted with a cyber attack at least once a week. Official statistics show that the most common threat vector was by far phishing attacks. Other threats include, but are not limited to ransomware, Distributed Denial of Service (DDoS) and Social engineering.

We offer services that can help build your organisation’s cyber resilience. For more information on the services we offer, please contact Martin Chapman or a member of the Forensics team.

Did you know…That the latest Cyber Security Breaches Survey found that 82% of businesses reported cyber security as a high priority for senior management, but only 19% of businesses have a formal incident response plan. |

CaaS has allowed individuals with little to no technical expertise to carry out complex attacks, which has contributed to the significant increase in cyber incidents globally.

CaaS refers to the provision of cybercriminal tools, services, and infrastructure on a commercial basis, typically on the dark web. Just as legitimate SaaS platforms offer cloud-based software on a subscription basis, CaaS providers offer a range of products that facilitate various forms of cybercrime. These can include:

The availability of CaaS has provided individuals with little to no technical expertise and the ability to carry out complex attacks, which has contributed to the significant increase in cyber incidents globally. The impact of CaaS includes the following:

CaaS represents a significant evolution in the threat landscape, making cybercrime more accessible and potentially more damaging. As this model continues to grow, it is crucial for businesses, individuals, and governments to stay ahead of the curve by implementing comprehensive cyber resilience strategies to fight against cybercrime.

For more information on the Forensic services we offer at Crowe, please contact Tim Robinson.

Did you know…CaaS businesses are marketed and sold in a manner like legitimate businesses, with customer support, refund policies, user-friendly interfaces, and subscription models that allow cybercriminals to scale their operations easily. |

In recent years, the rise of cybercrime has posed significant challenges to institutions worldwide, with healthcare systems being prime targets. The recent cyber-attack on the National Health Service (NHS) is estimated to be its biggest leak of patient data in years, highlighting the escalating threat and severe implications of such breaches.

On Thursday 20 June 2024, Russian-speaking cyber-crime group “Qilin” uploaded 104 files containing almost 400GB of private medical data from several NHS London hospitals to the dark web. The group claimed to have stolen the data from Synnovis, a pathology laboratory which processes blood tests on behalf of the NHS.

The current statement on NHS England website details that the ransomware attack in which this data was stolen took place on Monday 3 June 2024, with the National Crime Agency and National Cyber Security centre currently working to verify the data included in the published files. Qilin had reportedly been demanding a $50m (£40m) ransom.

Since the hacking, the NHS has faced significant disruption; appointments have been cancelled, overall services interrupted and planned surgeries postponed. Hospitals and GP surgeries infected by the ransomware are estimated to only be able to carry out 30% of their usual number of blood tests. Additionally, it doesn’t appear that there will be a quick resolution, with the NHS acknowledging that “full technical restoration will take some time, and the need to re-book tests and appointments will mean some disruption from the cyber incident will be felt over coming months.”

Cyber-attacks on healthcare systems like the NHS are particularly dangerous due to the sensitive nature and large amount of medical data they hold, and the critical services provided. When cybercriminals infiltrate these systems, they can disrupt hospital operations, delay medical procedures, and compromise patient care. Ransomware attacks, where hackers encrypt data and demand a ransom for its release, are especially disruptive. These attacks can cripple entire networks, forcing hospitals to revert to manual operations and risking patient safety. On top of this, the theft of personal and medical data can lead to identity theft and financial fraud, further endangering affected individuals. The potential for such data to be sold on the dark web only exacerbates the risks.

It is due to this potential significant and wide-reaching damage that the healthcare industry has become increasingly attractive to cybercriminals, who are eager to cause as much disruption as possible to ensure their ransom is paid. Evidence of this came last month, when the CEO of a top-10 Fortune 500 healthcare company confirmed they had paid a $22m (£17m) ransom in an attempt to protect stolen patient data.

This recent attack on the NHS highlights the growing sophistication of these types of attacks. Cyber criminals have evolved to employing business-like models that involve strategic planning, structured hierarchies, and advanced technologies. This development has enabled them to execute more large-scale and targeted attacks on vulnerable organisations like the NHS, who they see as more likely to pay the ransom. The financial motivation behind these ransomware attacks makes healthcare organisations a prime target for cybercriminals and represents a significant challenge for healthcare organisations around the globe. For more information contact Tim Robinson or your usual Crowe contact.

Did you know…Recent reports indicate that 81% of UK healthcare providers experienced ransomware attacks in 2022, a stark reminder of the vulnerabilities within the system. |