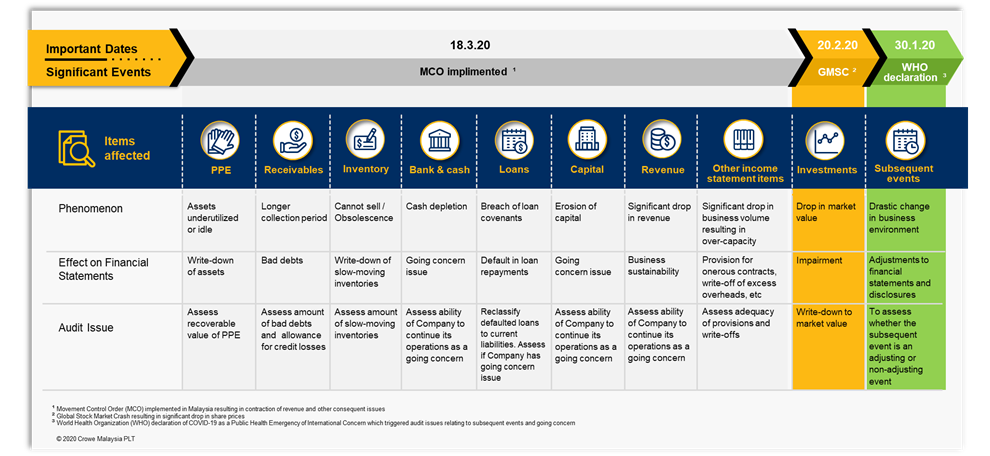

Impairment of non-financial assets e.g. buildings and equipment

To identify indications of impairment, changes in key drivers and assumptions used in estimating the recoverable amounts of the productive assets.

Provision for onerous contracts

A provision is required when unavoidable costs of meeting the obligations exceed the benefits expected to be received under the contract.

Foreign exchange transactions

To consider the effects of significant fluctuations in foreign exchange rates on the operations of the Company and the effectiveness of hedge accounting.

Inventories

To identify changes in net realisable values due to the decrease in selling prices or due to obsolescence.

Going concern

Material uncertainties may cast significant doubt on the ability of the Company to continue as a going concern.

Government support

To determine the appropriate accounting treatment of government support e.g. Economic Stimulus Package is a government grant that should be accounted for under MFRS 120 ‘Accounting for Government Grants and Disclosure of Government Assistance’.

Fixed production overheads

A higher amount of unallocated fixed overheads has to be expensed off due to abnormal production capacity / low production volume.

Disclosures in financial statements

More comprehensive disclosure is required of significant accounting judgments, estimates and assumptions used in preparing the financial statements that could result in material adjustments to the carrying amount of assets and liabilities.

Events after the reporting date

To carefully evaluate whether information on COVID-19 that becomes available after the reporting date is an adjusting or non-adjusting event for accounting purposes. Financial statements have to be updated if the event is a significant adjusting event; otherwise, a disclosure is required.

Lease contracts

To identity and account for any lease rent concessions.

Impact on auditor’s report

To evaluate whether the impact of COVID-19 is a Key Audit Matter. Depending on resolution of accounting and auditing matters due to COVID-19, possibilities exist as to whether it is necessary for the issuance of a modified opinion or inclusion of a separate section under ‘Material Uncertainty Related to Going Concern (MUGC)’ in the audit report.

Revenue contracts

Material uncertainties may cast significant doubt on the ability of the Company to continue as a going concern.

Receivables

Greater judgment is needed in assessing the expected credit loss.

Fair value of unquoted equity instruments

To update key drivers and assumptions used in the valuation techniques to reflect current market conditions at the reporting date.

Breach of loan covenants

To consider how a breach of loan covenant may affect the timing of repayment of the defaulted loan (e.g. the loan becomes repayable on demand) and how it affects the classification of the related liabilities at the reporting date. This also affects the assessment of the company’s ability to continue to operate as a going concern.