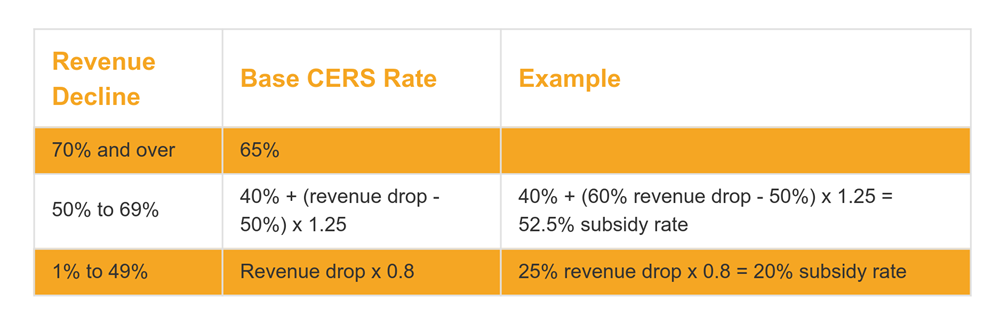

The elections and methods chosen by an eligible entity in determining its revenue for CERS must be consistent with those used for purposes of the CEWS and must be adopted for all three current periods of the CERS.

There is an additional 25 per cent “rent top-up percentage” available in respect of a location that has been forced to temporarily close or has seen certain activities, that would otherwise comprise approximately 25 per cent of the revenues of that location, completely cease for at least a week because of a COVID-19 public health order. If a location must temporarily close or sees certain activities cease for part of a qualifying period, the subsidy will be prorated in that period for the number of affected days. The government has provided some examples where a location would or would not be eligible for the “rent top-up percentage”.

The rate determined for a claim period, including any applicable “rent top-up percentage”, is multiplied by the total amount of “eligible expenses” for a location. Where a location is rented by an eligible entity, eligible expenses will include:

- gross rent,

- rent based on a percentage of sale or profit,

- amounts paid under a net lease as base rent,

- regular instalments of operating expenses (i.e. insurance, utilities, and common area maintenance),

- property and similar taxes (including school and municipal taxes),

- regular instalments of other amounts paid to the lessor for ancillary services customarily supplied in connection with real or immovable property; and

- amounts received by the lessor under the CERCA program that were applied to rent payable in the period.

Where the location is owned by an eligible entity, eligible expenses will include property insurance and interest on a commercial mortgage.

Eligible expenses cannot exceed $75,000 per location and there will be a maximum limit of $300,000 that must be shared by all affiliated entities in a qualifying period. Finally, eligible expenses must be paid to an arm’s length party pursuant to a written agreement entered before October 9, 2020. Mortgage interest on a property used to earn rental income from arm’s length parties will not qualify, nor will sales taxes, damages, interest and penalties and payments for special services.

- had a payroll account as of March 15, 2020 or were using a payroll service provider;

- had a business number as of September 27, 2020; or

- meet other conditions that may be prescribed in the future.

How Can Crowe Soberman Support You?

In these uncertain times, it is essential to remain agile and proactive as the COVID-19 situation unfolds. Having timely access to financial experts, insights and news as quickly as possible is critical—and that’s where we can help.

We have established a dedicated COVID-19 Resource Hub, highlighting areas of business operations that will likely be impacted by coronavirus. Whether you need to discuss your current financial situation and learn what options are available to you, or you want to be guided through the appropriate cash flow management strategies for your business, our team of experts are ready to help you at every step of the way. Please do not hesitate to reach out to your Crowe Soberman professionals for support during these challenging times.

We are in this together.

This article has been prepared for the general information of our clients. Please note that this publication should not be considered a substitute for personalized advice related to your situation.